Please review your YTD income in addition to your W2 income. Please consider 1) how much tax was paid in last year 2) how much tax you might owe on the additional income. A 20% on additional income for federal and 8% for state might be a safe net for potential estimated tax penalty and interests.

Here are some simple things taxpayers can do throughout the year to make next filing season less stressful.

Organize tax records. Create a system that keeps all important information together. Taxpayers can use a software program for electronic recordkeeping or store paper documents in clearly labeled folders. They should add tax records to their files as they receive them. Organized records will make tax return preparation easier and may help taxpayers discover overlooked deductions or credits.

Check withholding. Since federal taxes operate on a pay-as-you-go basis, taxpayers need to pay most of their tax as they earn income. Taxpayers should check that they’re withholding enough from their pay to cover their taxes owed, especially if their personal or financial situations change during the year. To check withholding, taxpayers can use the IRS Tax Withholding Estimator. If they want to change their tax withholding, taxpayers should provide their employer with an updated Form W-4.

Save for retirement. Saving for retirement can also lower a taxpayer’s AGI. Certain contributions to a retirement plan at work and to a traditional IRA may also reduce taxable income.

Many taxpayers file their federal tax returns and then eagerly anticipate details about their refund.

The best way to check the status of a refund is through the Where’s My Refund? tool, the IRS2Go app, or by signing in to the taxpayer’s IRS Online Account. But many people mistakenly think there are better ways to get their refund status. Here are some of the myths about tax refunds.

Myth: Calling the IRS, a tax software provider or a tax professional will provide a more accurate refund date.

Many people think talking to the IRS, tax software provider or their tax professional is the best way to find out when they will get their refund. There is no need to call the IRS unless Where’s My Refund? says to do so.

Taxpayers that do want refund info by phone can call the automated refund hotline at 800-829-1954. This hotline has the same information as the Where’s My Refund? tool.

Myth: Ordering a tax transcript is a secret way to get a refund date

A tax transcript will not help taxpayers find out when they will get their refund. IRS tools like Where’s My Refund? will tell taxpayers if their refund is approved and sent.

Myth: Where’s My Refund? must be wrong because there’s no deposit date yet

Where’s My Refund? on both IRS.gov and the IRS2Go mobile app are updated once a day, usually at night. Even though the IRS issues most refunds within 21 days, it’s possible a refund may take longer. Taxpayers should also consider the time it takes for the banks to post the refund to their account. People waiting for a refund in the mail should plan for the time it takes a check to arrive. If the IRS needs more information to process a tax return, the agency will contact the taxpayer by mail.

Myth: Where’s My Refund? must be wrong because the refund amount is less than expected

There are several factors that could cause a tax refund to be less than expected. The IRS will mail the taxpayer a letter of explanation if any adjustments are made. Some taxpayers may also receive a letter from the Department of Treasury’s Bureau of the Fiscal Service if their refund was reduced to offset certain financial obligations. Before calling, check Where’s My Refund or wait for the letter to understand why the change was made. The letter will also tell the taxpayers know how to respond, if they need to.

Myth: Getting a refund this year means there’s no need to adjust withholding for 2025

To help avoid a surprise next year, taxpayers should make changes now to prepare for next year. One way to do this is to adjust their tax withholding with their employer. The IRS Tax Withholding Estimator tool can help taxpayers determine if their employer is withholding the right amount.

Taxpayers who experience a life event like marriage, divorce, the birth or adoption of a child or no longer being able to claim a person as a dependent are encouraged to check their withholding. Taxpayers can use the results from the Tax Withholding Estimator to complete and submit a new Form W-4, Employee’s Withholding Certificate, to their employer as soon as possible. Withholding takes place throughout the year, so it’s better to take this step now.

New York State (NYS) and New York City (NYC) have implemented optional Pass-Through Entity Taxes (PTET) to help S corporations and other pass-through entities mitigate the federal $10,000 cap on state and local tax (SALT) deductions. By electing to pay taxes at the entity level, these businesses can provide their owners with a federal deduction for state and local taxes that would otherwise be limited.

New York State PTET:

Eligibility: Available to partnerships and New York S corporations for tax years beginning on or after January 1, 2021.

Benefits: Electing entities pay income tax at the entity level, allowing individual partners or shareholders to claim a PTET credit on their NYS personal income tax returns. This structure effectively bypasses the federal SALT deduction cap, enabling full deduction of state taxes at the federal level.

New York City PTET:

Eligibility: Available to city partnerships and city resident New York S corporations for tax years beginning on or after January 1, 2022.

Benefits: Similar to the state-level PTET, the NYC PTET allows electing entities to pay city taxes at the entity level. Shareholders who are NYC residents can then claim a credit against their NYC personal income tax liability, reducing their taxable income federally and circumventing the SALT deduction cap.

Considerations:

Election Process: The PTET election must be made annually and is irrevocable for that tax year once made. tax.ny.gov

Nonresident Implications: Nonresident partners or shareholders do not benefit from the NYC PTET, as the credit applies only to NYC residents.

Federal Deduction: By paying taxes at the entity level, the business can deduct these taxes federally, effectively working around the $10,000 SALT cap imposed on individual taxpayers. nysscpa.org

Electing into the NYS and NYC PTET can provide significant tax benefits by allowing S corporations to fully deduct state and local taxes at the federal level, thereby reducing overall tax liability.

Election Timing Requirements:

As of February 2025, the deadline for electing into the New York State (NYS) Pass-Through Entity Tax (PTET) for the 2025 tax year is March 15, 2025. This election must be made annually through the entity’s Business Online Services account. tax.ny.gov

However, there is proposed legislation under consideration that aims to extend the PTET election deadline to September 15 of the tax year. If enacted, this change would provide entities with additional time to assess their financial positions before making the election. taxnews.ey.com

It’s important to note that, as of now, this extension has not been finalized. Therefore, entities should plan to make their PTET election by the current deadline of March 15, 2025.

For the New York City (NYC) PTET, the election process and deadlines align with those of the NYS PTET. Eligible entities must opt in by March 15, 2025, through their Business Online Services account. tax.ny.gov

Given the potential for legislative changes, it’s advisable to consult with a tax professional or regularly check the New York State Department of Taxation and Finance website for the most current information regarding PTET election deadlines.

You may contact Us if you receive an IRS audit letter: Main Address: 200 Centennial Avenue, Suite 106, Piscataway, NJ 08854 Florida office: 14767 Lattice Ct, Jacksonville FL3226 Phone: (732) 896-0272 Email: cpa@cindiellc.com

What Triggers an IRS Audit? The IRS uses sophisticated computer algorithms to decide on which returns to audit. If your return looks strange, your chances of being audited go way up. Here are some reasons the IRS might audit you:

Taking Large Deductions – Returns with extremely large deductions in relation to income are more likely to be audited. For example, if your tax return shows that you earn $25,000, you are more likely to be audited if you claim $20,000 in deductions than if you claim $2,000.

Claiming Certain Kinds of Deductions – Certain types of deductions have long been thought to be hot buttons for the IRS, especially auto, travel, and meal expenses. Casualty losses and bad debt deductions might also increase your audit chances.

Claiming a Business Loss – Businesses that show losses are more likely to be audited, especially if the losses are recurring. The IRS might suspect that you must be making more money than you’re reporting—otherwise, why would you stay in business? Most likely to be audited are taxpayers reporting small business losses.

Claiming Deductions That Don’t Make Sense – Deductions that seem odd or out of character could increase your audit chances, like a plumber who deducts the cost of foreign travel might raise a few eyebrows at the IRS.

Not Reporting All of Your Income – The IRS also goes to great lengths to ensure you report all of your income. Its computers match the information on W-2s and 1099-NEC forms with the income amount reported on tax returns using Social Security and other identifying numbers. If the IRS finds discrepancies, it will probably start asking questions.

Having Evidence of Intent to Mislead or Being Sloppy With Your Return Filing a tax return with missing schedules or not providing all the information asked for on the forms can increase your chances of being audited. Similarly, a sloppy return, especially with math mistakes, increases your chances of an audit. Also, using round numbers—for example, $6,000 for business advertising costs or $4,000 for transportation expenses—indicates that you’re estimating, not using records to report amounts.

Being a Higher Earner – If you make over $500,000 per year, your audit likelihood is greater than the likelihood for the general population. As shown in the chart above, 0.7% of filers who earned between $500,000 and $1,000,000 were audited. So, Can I Get Away With Cheating on My Taxes? Even if you earn far less than $500,000, don’t think that you can easily get away with cheating on your taxes. (See “Are Increased IRS Audits Coming?” below.)

Having Self-Employment Income – The IRS tends to be suspicious of people in business for themselves. Depending on their income, sole proprietors are up to five times more likely to be audited than wage earners.

Having Foreign Accounts – Keeping money or other assets in foreign banks or other financial accounts increases audit chances.

Owning Digital Assets – Having digital assets, including cryptocurrency, such as Bitcoin, might increase your chances of an audit. IRS Form 1040 asks whether you received, sold, exchanged, or otherwise disposed of a digital asset during the year. If you say “yes,” your answer increases your audit chances.

Claiming Too Many Charitable Deductions – Claiming $20,000 in charitable deductions on your $50,000 salary will probably make the IRS suspicious. And if you don’t have documentation to back up your charitable deductions, don’t deduct them.

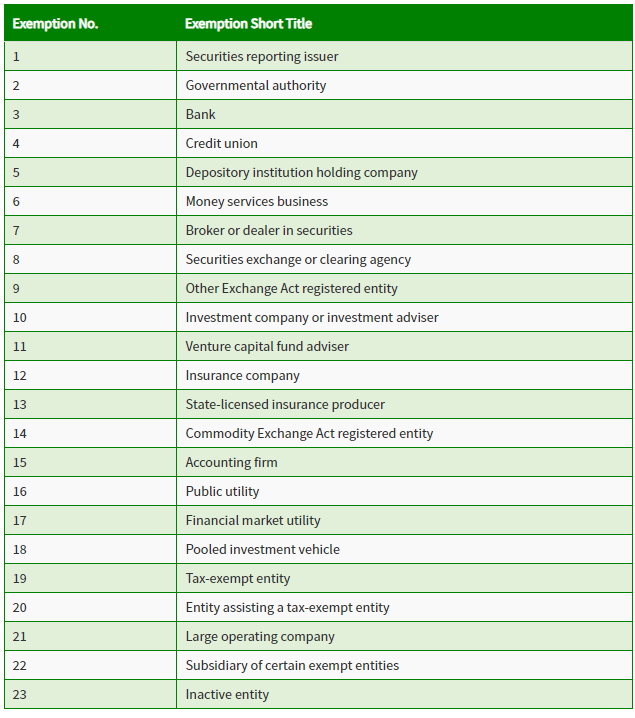

1. Securities reporting issuer: that is: (A) an issuer of a class of securities registered under Sec. 12 of the Securities Exchange Act of 1934, or (B) required to file supplementary and periodic information under Sec. 15(d) of the Securities Exchange Act of 1934.

2. Governmental authority:that: (A) is established under the laws of the United States, an Indian tribe, a State, or a political subdivision of a State, or under an interstate compact between two or more States, and (B) exercises governmental authority on behalf of the United States or any such Indian tribe, State, or political subdivision.

3. Bank:as defined in: (A) Sec. 3 of the Federal Deposit Insurance Act, (B) Sec. 2(a) of the Investment Company Act of 1940, or (C) Sec. 202(a) of the Investment Advisers Act of 1940.

4. Credit union:Federal credit union or State credit union, as those terms are defined in Sec. 101 of the Federal Credit Union Act.

5. Depository institution holding company: bank holding company as defined in Sec. 2 of the Bank Holding Company Act of 1956, or any savings and loan holding company as defined in Sec. 10(a) of the Home Owners’ Loan Act.

6. Money services business:money transmitting business registered with FinCEN under 31 U.S.C. 5330, and any money services business registered with FinCEN under 31 CFR 1022.380.

7. Broker or dealer in securities:broker or dealer, as those terms are defined in Sec. 3 of the Securities Exchange Act of 1934, that is registered under Sec. 15 of that Act.

8. Securities exchange or clearing agency:exchange or clearing agency, as those terms are defined in Sec. 3 of the Securities Exchange Act of 1934, that is registered under Secs. 6 or 17A of that Act.

9. Other Exchange Act registered entity:Any entity other than that described in exemption 1 (Securities reporting issuer), exemption 7 (Broker or dealer in securities), or exemption 8 (Securities exchange or clearing agency) that is registered with the SEC under the Securities Exchange Act of 1934.

10. Investment company or investment adviser:Any entity that is: (A) an investment company as defined in Sec. 3 of the Investment Company Act of 1940, or is an investment adviser as defined in Sec. 202 of the Investment Advisers Act of 1940, and (B) registered with the SEC under the Investment Company Act of 1940 or the Investment Advisers Act of 1940.

11. Venture capital fund adviser:Any investment adviser that: (A) is described in section 203(l) of the Investment Advisers Act of 1940, and (B) has filed Item 10, Schedule A, and Schedule B of Part 1A of Form ADV, or any successor thereto, with the SEC.

12. Insurance company:Any insurance company as defined in Sec. 2 of the Investment Company Act of 1940.

13. State-licensed insurance producer:Any entity that: (A) is an insurance producer that is authorized by a State and subject to supervision by the insurance commissioner or a similar official or agency of a State, and (B) has an operating presence at a physical office within the United States.

14. Commodity Exchange Act registered entity:Any entity that: (A) is a registered entity as defined in Sec. 1a of the Commodity Exchange Act, or (B) is: (1) a futures commission merchant, introducing broker, swap dealer, major swap participant, commodity pool operator, or commodity trading advisor, each as defined in Sec. 1a of the Commodity Exchange Act, or a retail foreign exchange dealer as described in Sec. 2(c)(2)(B) of the Commodity Exchange Act and (2) registered with the Commodity Futures Trading Commission under the Commodity Exchange Act.

15. Accounting firm:Any public accounting firm registered in accordance with Sec. 102 of the Sarbanes-Oxley Act of 2002.

16. Public utility:Any entity that is a regulated public utility as defined in 26 USC 7701(a)(33)(A) that provides telecommunications services, electrical power, natural gas, or water and sewer services within the United States.

17. Financial market utility:Any financial market utility designated by the Financial Stability Oversight Council under Sec. 804 of the Payment, Clearing, and Settlement Supervision Act of 2010.

18. Pooled investment vehicle:Any pooled investment vehicle that is operated or advised by a person described in exemptions 3 (bank), 4 (credit union), 7 (broker or dealer in securities), 10 (investment company or investment adviser), or 11 (venture capital fund adviser).

19. Tax-exempt entity:Any entity that is: (A) an organization that is described in Sec. 501(c) of the Internal Revenue Code of 1986 (determined without regard to Sec. 508(a) of the Code) and exempt from tax under Sec. 501(a) of the Code, except that in the case of any such organization that ceases to be described in Sec. 501(c) and exempt from tax under Sec. 501(a), such organization shall be considered to continue to be described as a tax-exempt entity for the 180-day period beginning on the date of the loss of such tax-exempt status, (B) a political organization, as defined in Sec. 527(e)(1) of the Code, that is exempt from tax under Sec. 527(a) of the Code, or (C) a trust described in paragraph (1) or (2) of Sec. 4947(a) of the Code.

20. Entity assisting a tax-exempt entity:Any entity that: (A) operates exclusively to provide financial assistance to, or hold governance rights over, any entity described in exemption 19 above (tax-exempt entity), (B) is a United States person, (C) is beneficially owned or controlled exclusively by one or more United States persons that are United States citizens or lawfully admitted for permanent residence, and (D) derives at least a majority of its funding or revenue from one or more United States persons that are United States citizens or lawfully admitted for permanent residence.

21. Large operating company:Any entity that: (A) employs more than 20 full time employees in the United States, with “full time employee in the United States” having the meaning provided in 26 CFR 54.4980H-1(a) and 54.4980H-3, except that the term “United States” as used in those sections of the CFR have the meaning provided in 31 CFR 1010.100(hhh), (B) has an operating presence at a physical office within the United States, and (C) filed a Federal income tax or information return in the United States for the previous year demonstrating more than $5,000,000 in gross receipts or sales, as reported as gross receipts or sales (net of returns and allowances) on the entity’s IRS Form 1120, consolidated IRS Form 1120, IRS Form 1120-S, IRS Form 1065, or other applicable IRS form, excluding gross receipts or sales from sources outside the United States, as determined under Federal income tax principles. For an entity that is part of an affiliated group of corporations within the meaning of 26 USC 1504 that filed a consolidated return, the applicable amount shall be the amount reported on the consolidated return for such group.

22. Subsidiary of certain exempt entities:Any entity whose ownership interests are controlled or wholly owned, directly or indirectly, by one or more entities described in exemptions 1, 2, 3, 4, 5, 7, 8, 9, 10, 11, 12, 13, 14, 15, 16, 17, 19, or 21 set forth above.

23. Inactive entity:Any entity that: (A) was in existence on or before January 1, 2020, (B) is not engaged in active business, (C) is not owned by a foreign person, whether directly or indirectly, wholly or partially, (D) has not experienced any change in ownership in the preceding twelve-month period, (E) has not sent or received any funds in an amount greater than $1,000, either directly or through any financial account in which the entity or any affiliate of the entity had an interest, in the preceding 12 month period, and (F) does not otherwise hold any kind or type of assets, whether in the United States or abroad, including any ownership interest in any corporation, limited liability company, or other similar entity.

This new rule mainly targets small businesses. Starting in 2024, newly established corporations, limited liability companies (LLCs), limited partnerships, and other entities filing formation documents with a state’s Secretary of State’s office (or similar government agency) must submit a report to the U.S. Treasury Department’s Financial Crimes Enforcement Network (FinCEN) detailing the entity’s “beneficial owners.” Entities existing before January 1, 2024, have until January 1, 2025, to comply with this requirement. This is called BOI reporting, or Beneficial Owner Information Reporting.

This regulation is part of the federal government’s efforts to combat money laundering and tax evasion by scrutinizing shell companies that conceal assets. However, it imposes significant reporting obligations on most businesses. Willful failure to provide or update the required information can result in hefty fines of up to $500 per day until the violation is corrected, or, if criminal charges are pursued, fines up to $10,000 and/or two years imprisonment. These penalties can apply to the beneficial owner, the entity, and/or the person completing the report. Beneficial owners are broadly defined as individuals who directly or indirectly own more than 25% of the entity’s ownership interests or exercise substantial control over the entity (even without ownership interest). This includes many senior officers and key decision-makers (e.g., board members). Given the severe penalties, it is safer to over-report rather than under-report beneficial owners. Entities formed after 2023 must also provide information about the company applicants (those filing the formation/registration papers and those directing the filing). The required information for beneficial owners includes their legal name, residential address, date of birth, and a unique identifier from a non-expired passport, driver’s license, or state identification card. An image of these documents must also be submitted to FinCEN.

23 types of entities are excepted from BOI filing: List

Entities formed before January 1, 2024, must file these reports by January 1, 2025. Entities formed in 2024 have 90 days from formation/registration to file, while those formed after 2024 must file within 30 days.

Any changes in the reported information, such as changes in a beneficial owner’s address or name, a new passport number, or an updated driver’s license, must be reported within 30 days to avoid penalties. It is crucial to discuss who qualifies as a beneficial owner in your business and establish systems to keep this information current. Please contact our office soon to schedule an appointment for further discussion.

Florida is known as one of the lowest-taxed states in the country in part because there is no state income tax. The state government largely funds its operations through fees, sales taxes and revenue from the federal government revenue from the federal government

While Florida does not tax personal income, it’s important to note that the state does place a levy on corporate profits. So if you own a company doing business in Florida, you may owe money to the state government.

Local governments in Florida also depend on property taxes for revenue. So even though there is no statewide property tax, you’ll want to consider these municipal costs when calculating the tax burden you’ll face in Florida.

A Florida resident’s primary residence is protected from levy and execution by their judgment creditors by Article X Section 4 of the Florida Constitution. Florida also provides its residents with statutory creditor protection for life insurance proceeds and cash value, annuities, retirement accounts, and wages. This helps foster peace of mind that certain of your assets are not as easily reached by creditors. For married couples, Florida recognizes the Tenancy by the Entireties (TBE) form of joint survivorship ownership over real and personal property. TBE property may be protected from the creditors of one spouse if the other spouse is not also a party to the underlying claim.

Obviously, if you spend more than half your time in Florida, you won’t reach the 183-day threshold in the state where you spend your summers. If you can’t spend that much time in Florida, then take a vacation, visit family or friends, or otherwise spend time in some other location — anything to avoid spending 183 days or more in your high-tax summer state.

What the right to challenge the IRS’s position and be heard means for you?

IRS is in actin. Many clients received letters from IRS. You have the right to take actions as well.

IRS wants every taxpayer to be know and understand their rights in the event they need to work with the IRS on a personal tax matter. These 10 fundamental rights are collectively known as the Taxpayer Bill of Rights. Included on this list is the right to challenge the IRS’s position and be heard. Here’s more about what this right means for you.

You have the right to:

Raise objections.

Provide additional documentation in response to formal or proposed IRS actions.

Expect the IRS to consider their timely objections.

Have the IRS consider any supporting documentation promptly and fairly.

Receive a response if the IRS does not agree with their position.

Here are some specific things this right affords:

In some cases, the IRS will notify you that their tax return has a math or clerical error. If this happens, the taxpayer:

Has 60 days to tell the IRS that they disagree.

Should provide copies of any records that may help correct the error.

May call the number listed on the letter or bill for assistance.

Can expect the agency to make the necessary adjustment to their account and send a correction if the IRS upholds the taxpayer’s position.

Here’s what will happen if the IRS does not agree with the taxpayer’s position:

The agency will issue a notice proposing a tax adjustment. This is a letter that comes in the mail.

This notice provides the taxpayer with a right to challenge the proposed adjustment.

You make this challenge by filing a petition in U.S. Tax Court. You must generally file the petition within 90 days of the date of the notice, or 150 days if it is addressed outside the United States.

You can submit documentation and raise objections during an audit. If the IRS does not agree with the your position, the agency issues a notice explaining why it is increasing the tax. Prior to paying the tax, the you have the right to petition the U.S. Tax Court and challenge the agency’s decision.

In some circumstances, the IRS must provide you with an opportunity to have hearing with the independent Office of Appeals before taking enforcement actions to collect tax debt. These actions include levying the your bank account immediately after filing a notice of federal tax lien in the appropriate state filing location. If the you disagree with the decision of the Appeals Office, they can petition the U.S. Tax Court.

The IRS developed the FBAR vs 8938 graph to assist taxpayers. The Internal Revenue Service prepares its own graph to compare the two forms, which may be of assistance to you. It has been reproduced below for you:

Form 8938, Statement of Specified Foreign Financial Assets

FinCEN Form 114, Report of Foreign Bank and Financial Accounts (FBAR)

Who Must File?

Specified individuals and specified domestic entities that have an interest in specified foreign financial assets and meet the reporting threshold-Specified individuals include U.S citizens, resident aliens, and certain non-resident aliens-Specified domestic entities include certain domestic corporations, partnerships, and trusts

U.S. persons, which include U.S. citizens, resident aliens, trusts, estates, and domestic entities that have an interest in foreign financial accounts and meet the reporting threshold

Does the United States include U.S. territories?

No

Yes, resident aliens of U.S territories and U.S. territory entities are subject to FBAR reporting

Reporting Threshold (Total Value of Assets)

Specified individuals living in the US:-Unmarried individual (or married filing separately): Total value of assets was more than $50,000 on the last day of the tax year, or more than $75,000 at any time during the year.-Married individual filing jointly: Total value of assets was more than $100,000 on the last day of the tax year, or more than $150,000 at any time during the year.Specified individuals living outside the US:-Unmarried individual (or married filing separately): Total value of assets was more than $200,000 on the last day of the tax year, or more than $300,000 at any time during the year.-Married individual filing jointly: Total value of assets was more than $400,000 on the last day of the tax year, or more than $600,000 at any time during the year.Specified domestic entities:Total value of assets was more than $50,000 on the last day of the tax year, or more than $50,000 at any time during the tax year.

Aggregate value of financial accounts exceeds $10,000 at any time during the calendar year. This is a cumulative balance, meaning if you have 2 accounts with a combined account balance greater than $10,000 at any one time, both accounts would have to be reported.

When do you have an interest in an account or asset?

If any income, gains, losses, deductions, credits, gross proceeds, or distributions from holding or disposing of the account or asset are or would be required to be reported, included, or otherwise reflected on your income tax return

Financial interest: you are the owner of record or holder of legal title; the owner of record or holder of legal title is your agent or representative; you have a sufficient interest in the entity that is the owner of record or holder of legal title.Signature authority: you have authority to control the disposition of the assets in the account by direct communication with the financial institution maintaining the account.See instructions for further details.

What is Reported?

Maximum value of specified foreign financial assets, which include financial accounts with foreign financial institutions and certain other foreign non-account investment assets

Maximum value of financial accounts maintained by a financial institution physically located in a foreign country

How are maximum account or asset values determined and reported?

Fair market value in U.S. dollars in accord with the Form 8938 instructions for each account and asset reportedConvert to U.S. dollars using the end of the taxable year exchange rate and report in U.S. dollars.

Use periodic account statements to determine the maximum value in the currency of the account.Convert to U.S. dollars using the end of the calendar year exchange rate and report in U.S. dollars.

When Due?

Form is attached to your annual return and due on the date of that return, including any applicable extensions

Received by April 15 (6-month automatic extension to Oct 15)

Where to File?

File with income tax return pursuant to instructions for filing the return.

File electronically through FinCENs BSA E-Filing System. The FBAR is not filed with a federal tax return.

Penalties

Up to $10,000 for failure to disclose and an additional $10,000 for each 30 days of non-filing after IRS notice of a failure to disclose, for a potential maximum penalty of $60,000; criminal penalties may also apply

Civil monetary penalties are adjusted annually for inflation. For civil penalty assessment prior to Aug 1, 2016, if non-willful, up to $10,000; if willful, up to the greater of $100,000 or 50 percent of account balances; criminal penalties may also apply

Types of Foreign Assets and Whether They are Reportable

Financial (deposit and custodial) accounts held at foreign financial institutions

Yes

Yes

Financial account held at a foreign branch of a U.S. financial institution

No

Yes

Financial account held at a U.S. branch of a foreign financial institution

No

No

Foreign financial account for which you have signature authority

No, unless you otherwise have an interest in the account as described above

Yes, subject to exceptions

Foreign stock or securities held in a financial account at a foreign financial institution

The account is subject to reporting, but the contents of the account do not have to be separately reported

The account itself is subject to reporting, but the contents of the account do not have to be separately reported

Foreign stock or securities not held in a financial account

Yes

No

Foreign partnership interests

Yes

No

Indirect interests in foreign financial assets through an entity

No

Yes, if sufficient ownership or beneficial interest (i.e., a greater than 50 percent interest) in the entity. See instructions for further detail.

Foreign mutual funds

Yes

Yes

Domestic mutual fund investing in foreign stocks and securities

No

No

Foreign accounts and foreign non-account investment assets held by foreign or domestic grantor trust for which you are the grantor

Yes, as to both foreign accounts and foreign non-account investment assets

Yes, as to foreign accounts

Foreign-issued life insurance or annuity contract with a cash-value

Yes

Yes

Foreign hedge funds and foreign private equity funds

Yes

No

Foreign real estate held directly

No

No

Foreign real estate held through a foreign entity

No, but the foreign entity itself is a specified foreign financial asset and its maximum value includes the value of the real estate

No

Foreign currency held directly

No

No

Precious Metals held directly

No

No

Personal property, held directly, such as art, antiques, jewelry, cars and other collectibles

No

No

‘Social Security’- type program benefits provided by a foreign government

No

No

*Note – This table is current through the publication date. Please check the instructions for each form for information regarding any future developments.

Higher Income /Making a lot of Money: Biden’s Build Back Better bill – high-wealth exam squad at work- 1040 related business returns – domestic and foreign. IRS says $400K income and below is safe though.

High than average deductions, losses or credits: But if you have the proper documentation for your deduction, loss or credit, don’t be afraid to claim it.:

Take Larger than average Charitable Deductions based on the income level

Running a business on Schedule C: 100K or Cash-intensive

Non-filers: $100K and above failed filing

Claiming the American Opportunity Tax Credit on Form 8863

Taking an Early Payout from an IRA or 401(k) Account without paying 10% penalty

Change in Alimony Deductions

Cash Transactions: Reports from other agencies or financial institutions

Failing to Report a Foreign Bank Account: foreign accounts that combined total more than $10,000 at any time. FinCEN Report 114 (FBAR) and Form 8938

Claiming the Foreign Earned Income Exclusion

Business:

Claiming rental losses

Hobby vs Business

Claiming 100% Business Use of a Vehicle on Form 4562: Be sure to have 2nd car for personal use.

Claiming Day-Trading Losses on Schedule C

Operating a Marijuana Business

Taking the Research & Development Credit

Failing Report Certain Professional Earnings as Self-Employment Income: Not an investor